Compliance functions inside global banks and insurers are buckling under cost. Regulators keep expanding the perimeter — sanctions lists refresh weekly, KYC refresh cycles compress, AML scenarios multiply, and reporting templates change every quarter — while headcount budgets at the parent stay flat or shrink. The buyer pain is simple: compliance teams are spending more to stand still, and the audit committee is asking why technology hasn't bent the curve.

The Global Capability Centre in India has emerged as the answer most large financial institutions are converging on. Not as a cost-arbitrage call centre running alerts, but as the parent's centre of excellence for RegTech — owning the platforms, the models, the integrations and increasingly the regulatory interpretation itself.

The shift from back-office to RegTech CoE

For two decades the India GCC was a processing site. Alert dispositioning, KYC document indexing, regulatory return preparation — work measured in tickets closed and SLAs met. That model is over for any bank or insurer with a serious compliance footprint.

The second-generation GCC is an engineering function. It builds and runs the transaction monitoring engine that sits across the group's payment rails. It owns the sanctions screening platform that every onboarding journey calls. It maintains the regulatory reporting factory that files FATCA, CRS, Basel III/IV, MIFID II, IFRS 17, RBI returns and IRDAI submissions on cadence. The compliance officers at the parent define policy; the GCC turns policy into running code.

What changed is the talent supply and the technology stack converging in the same geography at the same time. India has the largest concentration of regulator-aware engineering talent anywhere — people who have shipped real AML platforms, real KYC orchestration layers, real Basel calculators — and the same metros now have deep benches in machine learning, graph analytics and cloud-native data engineering. That combination doesn't exist at scale anywhere else.

Why the GCC model fits RegTech specifically

RegTech is the rare workload where the GCC structural advantages line up almost perfectly with what the function actually needs.

Compliance technology is long-lived. An AML platform built today will run for ten to fifteen years with continuous tuning. Vendor outsourcing creates lock-in and an annuity for the vendor; the captive GCC model keeps the intellectual property, the model weights, the scenario library and the institutional knowledge inside the enterprise.

Regulators increasingly flag concentration risk. Running critical compliance infrastructure from a single site — typically the parent country — is becoming a finding in supervisory reviews. A second engineering site in a different jurisdiction, time zone and risk geography is now a resilience requirement, not a cost play.

The economics still matter. Building the same RegTech engineering function at the parent costs roughly two to three times what it costs to run from a Noida, Bengaluru, Hyderabad or Pune captive. The savings don't come from paying less for the same person — they come from being able to staff a larger, more specialised team for the same budget. A bank that could afford twelve compliance engineers in London can run a forty-person platform team in India, with model risk, data engineering, DevSecOps and regulatory analyst capability all in-house.

And the AI talent question has flipped. Five years ago, "we need GenAI for compliance" pointed at California. Today the largest production deployments of LLM-assisted KYC narrative generation, adverse media screening and sanctions name-matching are being built inside Indian GCCs. The talent is here, the cost to experiment is lower, and the willingness to ship is higher.

What a RegTech-focused GCC actually delivers

The deliverables are concrete and they map directly to line items the chief compliance officer already pays for somewhere — usually to three or four different vendors.

Transaction monitoring and AML

A real-time monitoring engine that ingests every payment, card and account event across the group, scores it against a configurable scenario library, and routes alerts to a case management workflow. The differentiator is the tuning loop — the GCC team owns the false-positive reduction work, retunes thresholds quarterly, A/B tests new scenarios in shadow mode, and reports model performance to the audit committee. This is the kind of long-running optimisation work that vendors will not do for you.

Sanctions, PEP and adverse media screening

A screening layer that sits in front of onboarding, payments and periodic refresh. Multi-list, multi-vendor data aggregation. Fuzzy matching tuned per jurisdiction. Adverse media ingestion with LLM-assisted relevance scoring. The hard problem is not the match engine — it's the disposition workflow and the model governance around it, which the GCC owns end-to-end.

KYC, CDD and periodic refresh

An orchestration layer that pulls from multiple bureaus and government data sources, routes documents through OCR and verification, escalates risk-flagged cases to enhanced due diligence, and triggers refresh on the regulator-mandated cycle. For institutions that have already invested in a policy administration platform or core banking system, the GCC builds the KYC orchestration as a service the platforms call.

Regulatory reporting

A reporting factory that handles FATCA and CRS files, Basel III/IV calculations, MIFID II transaction reporting, IFRS 17 disclosure templates, RBI returns for India entities, IRDAI submissions for insurance, and the equivalent in every market the parent operates in. The win is the shared data model — once the source-system feeds are landed in a regulatory data lake, adding a new report becomes weeks not months.

Audit trail, case management and model governance

The unglamorous but audit-critical layer. Immutable audit logs across every compliance decision. Case management with SLA tracking and four-eyes workflow. Model risk documentation, version control, challenger model results and validation reports — increasingly demanded by supervisors as machine learning enters more compliance decisions.

The build sequence — how to stand one up

The temptation is to spend nine months on entity setup, real estate and a hiring plan before writing a line of code. That is the old GCC playbook and it is the wrong one for RegTech.

The right sequence overlaps the build:

- Month 0 to 2 — entity selection, registered office, statutory filings, and a managed-services bridge so a Redian-led pod is already shipping the first compliance workload before the captive payroll is live.

- Month 2 to 4 — anchor hires for the platform leadership, compliance engineering lead, data engineering lead, model risk lead. Real estate or hub-and-spoke decision finalised.

- Month 4 to 9 — scaled hiring against a defined platform roadmap, gradual transition of the managed-services pod into the captive, first regulatory workload in production.

- Month 9 to 18 — second and third workloads migrate, GCC takes over change management from parent vendors, audit committee starts seeing GCC metrics directly.

This is the model we run on GCC engagements — entity, hiring, infrastructure and security operational by month three, with a Redian-led staff augmentation bridge that converts to your captive payroll on your timeline. The handover is contractual, not aspirational.

Where this lands for banks versus insurers

The workload mix differs by sector but the GCC structure is the same.

Banks lead with AML transaction monitoring, sanctions screening, KYC refresh and Basel reporting. The integration surface is the core banking system, the payment switches and the customer onboarding journeys — work that pairs naturally with digital banking channels and loan management modernisation programmes already underway.

Insurers lead with sanctions screening at issuance, beneficiary screening at claims, IFRS 17 reporting, IRDAI/regulator returns and increasingly model governance around ML-driven pricing engines and claims automation. The GCC also tends to absorb broker compliance work for groups running an intermediary channel.

In both sectors, the GCC becomes the single throat to choke for regulatory technology — replacing a patchwork of vendor contracts and parent-country engineering with one owned capability.

What the audit committee should expect

A well-run RegTech GCC reports on four things, quarterly, in language the board understands.

False-positive rates on monitoring and screening, trending down. Time-to-disposition on alerts, trending down. Cost-per-alert and cost-per-regulatory-report, trending down. Coverage — number of jurisdictions, products and regulatory regimes the platform supports, trending up. When those four lines start moving in the right direction the GCC has earned its place; until they do, it is still a cost centre.

The board should also expect the GCC to own the regulatory horizon-scanning function. New rule on the way? The GCC team has read the consultation paper, scoped the impact, and put a delivery plan on the table before the local compliance officer asks for one.

Build with Redian

We have stood up India GCCs for banks and insurers operating across the UK, Africa, the Gulf and South Asia, and we run the BFSI delivery practice that does the engineering work inside them. The combination — captive setup plus the regulated-industry engineering bench to populate it — is rare. If you are scoping a RegTech GCC or trying to convert an existing back-office captive into one, start a conversation with our team.

Stay current with our insights

One monthly email. Banking, insurance, AI/ML and CRM field notes. No spam.

We respect your privacy. Read our Privacy Policy.

Keep reading

More from GCCs

GCCs

India GCCs — from back office to innovation hub

India's Global Capability Centres have moved beyond cost arbitrage. Here is what the next generation looks like.

08 Apr 2026

Banking

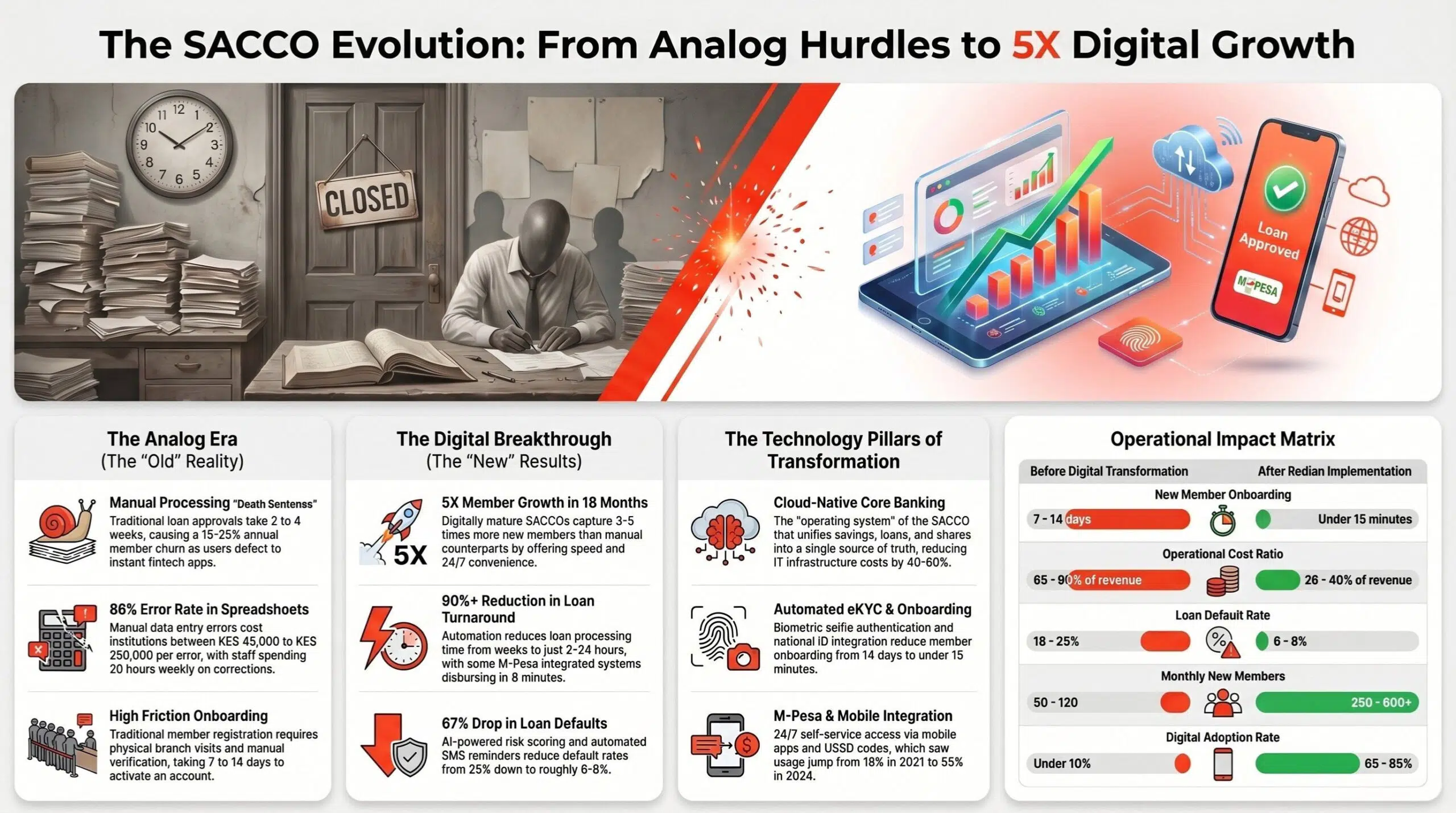

SACCO management system — Kenya's credit unions achieve 5× member growth

How Kenya's credit unions are achieving 5× member growth in 18 months with digital-first SACCO management. The architecture, the playbook and the numbers.

28 May 2026

Insurance

Insurance broker management — from policy to profit in 2026

A practical guide to what a modern broker management system has to do — and how to evaluate one.

22 May 2026

Build with Redian

Have a similar build in mind?

We've shipped gccs systems for banks, insurers, brokers, MFIs, SACCOs and enterprises across the USA, UK, Africa, UAE and India. Book a 30-min call with a senior engineer — no pitch deck, just a sharp first read on your initiative.

- CMMI Level 3 Appraised · ISO Certified delivery

- 1 business day response · NDA on request

- Senior engineers, not sales — first call