From Core Banking to Digital Channels: How Redian Software Empowers Financial Institutions in Cameroon

Redian Software empowers banks and microfinance institutions in Cameroon with core banking, loan management, mobile apps, USSD, and digital banking solutions.

Cameroon’s financial services sector is at a critical inflection point. Rapid growth in mobile usage, increasing demand for digital payments, and the rise of fintech innovation are reshaping how banks, microfinance institutions, and lenders operate and compete. Customers today expect speed, transparency, and access — whether through smartphones, USSD, or web platforms — while regulators demand stronger controls, reporting, and risk management.

Yet many financial institutions still rely on fragmented legacy systems, manual processes, and disconnected channels that limit agility and growth. Core banking platforms operate in isolation, loan processing is slow and paper-heavy, and customer engagement is constrained to physical branches. This gap between operational reality and digital expectation creates inefficiencies, higher costs, and missed opportunities for financial inclusion.

Financial institutions in Cameroon commonly face:

- Fragmented legacy systems and manual workflows (Excel-driven back offices).

- Limited digital access for customers in rural and semi-urban areas.

- Complex regulatory and compliance demands across transactions and lending.

- High operational costs, slow loan processing, and limited customer analytics.

These constraints reduce competitiveness and slow financial inclusion — unless addressed by an integrated technology strategy.

- Scalable core banking engine supporting deposits, accounts, transaction posting, and GL integration.

- Specialized loan management with configurable products, interest models, collateral tracking, repayment schedules, and provisioning workflows — built for both commercial banks and microfinance institutions.

- Integration-ready architecture so existing channels, payment gateways, and regulatory reporting tools can be connected without ripping everything out.

- Mobile App & Web Portal: Full self-service for onboarding, account management, transfers, statements, and loan applications — with layered KYC and secure authentication.

- USSD: Low-bandwidth, widely accessible channel for account enquiries, mini-statements, and simplified payments — critical for rural reach.

- API-first design: Enables partners (payment gateways, aggregators, credit bureaus) and third-party fintechs to integrate rapidly.

###

- Payment integrations: Local payment providers, mobile money operators, and card schemes.

- Regulatory/reporting: Automated feeds for compliance, tax authorities, and central bank reporting formats.

- Analytics & dashboards: Real-time KPIs for deposit growth, NPLs, portfolio-at-risk, and product performance.

- Rapid digitization without disruption: An integration-first strategy lets institutions keep mission-critical operations running while modernizing incrementally.

- Inclusion-first channels: USSD + mobile apps let banks reach thin-file customers and rural populations cost-effectively.

- Product flexibility: Configurable loan products enable quicker go-to-market for promos, salary loans, agricultural credit, and microloans.

- Local delivery expertise: Redian’s hands-on implementations in Cameroon lower deployment risk and shorten the learning curve for local teams.

Stay current with our insights

One monthly email. Banking, insurance, AI/ML and CRM field notes. No spam.

We respect your privacy. Read our Privacy Policy.

Keep reading

More from Banking

Banking

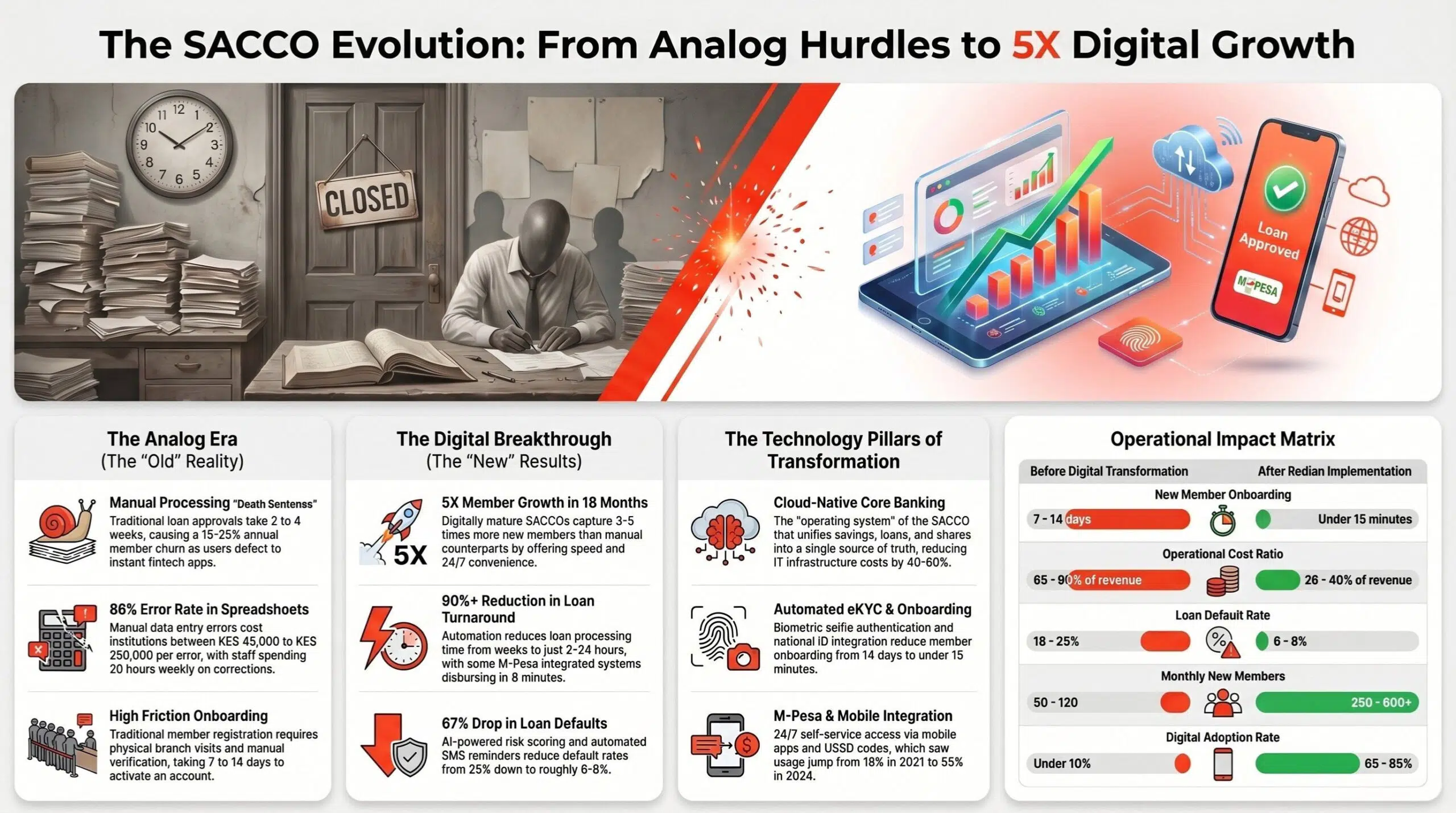

SACCO management system — Kenya's credit unions achieve 5× member growth

How Kenya's credit unions are achieving 5× member growth in 18 months with digital-first SACCO management. The architecture, the playbook and the numbers.

28 May 2026

Banking

Why SACCOs in Africa must adopt digital core banking — now

Member expectations have moved faster than legacy core systems. A practical case for digital core banking in the SACCO movement.

15 Apr 2026

Banking

What Microfinance Institutions, NBFCs & Cooperatives in Southeast Asia Must Learn in 2025 — and How to Build a Winning Digital Strategy for 2026

Learn how microfinance institutions, NBFCs, and cooperatives in Indonesia, Vietnam, Malaysia, and the Philippines can build a scalable, compliant digital strategy for 2026.

26 Dec 2025

Build with Redian

Have a similar build in mind?

We've shipped banking systems for banks, insurers, brokers, MFIs, SACCOs and enterprises across the USA, UK, Africa, UAE and India. Book a 30-min call with a senior engineer — no pitch deck, just a sharp first read on your initiative.

- CMMI Level 3 Appraised · ISO Certified delivery

- 1 business day response · NDA on request

- Senior engineers, not sales — first call