Africa has more than 350 million unbanked adults — over half the eligible population — sitting on the wrong side of a credit gap that traditional banking has never closed. The reasons are familiar: branch networks that stop at the city limits, collateral requirements that exclude anyone without title deeds, and approval cycles measured in weeks. Digital lending platforms are rewriting that equation, and the institutions that build them well are now defining the next decade of African finance.

The exclusion that built the opportunity

Formal lending in Africa has historically been a closed door for most small businesses and individuals. Underwriting standards were written for salaried borrowers with documented employment histories. Paperwork demands assumed access to a notary, a printer, and time off work. Interest rates priced in the cost of physical distribution, and collateral expectations — buildings, land, registered vehicles — ruled out the very entrepreneurs driving the informal economy.

The result was a structural void. Globally, 1.7 billion adults lack basic financial services, and Africa carries a disproportionate share of that figure. Yet the same continent leapfrogged landlines for mobile, then leapfrogged plastic for mobile money. By 2023, mobile penetration had reached 61 percent while only 54 percent of African adults held a formal bank account — a gap that signalled exactly where the next generation of credit had to be delivered.

That signal has been read clearly by fintechs, regulators, and the technology partners building behind them. The African fintech industry is now the continent's fastest-growing startup sector, projected to grow thirteenfold to roughly US$65 billion by 2030 at a 32 percent CAGR, with South Africa, Nigeria, Egypt, and Kenya leading. Broader fintech revenues are tracking toward $230 billion by 2025 at a 10 percent annual growth rate. For lenders, insurers, and the platforms that serve them, this is the largest greenfield credit market on earth.

How digital lending platforms changed the rules

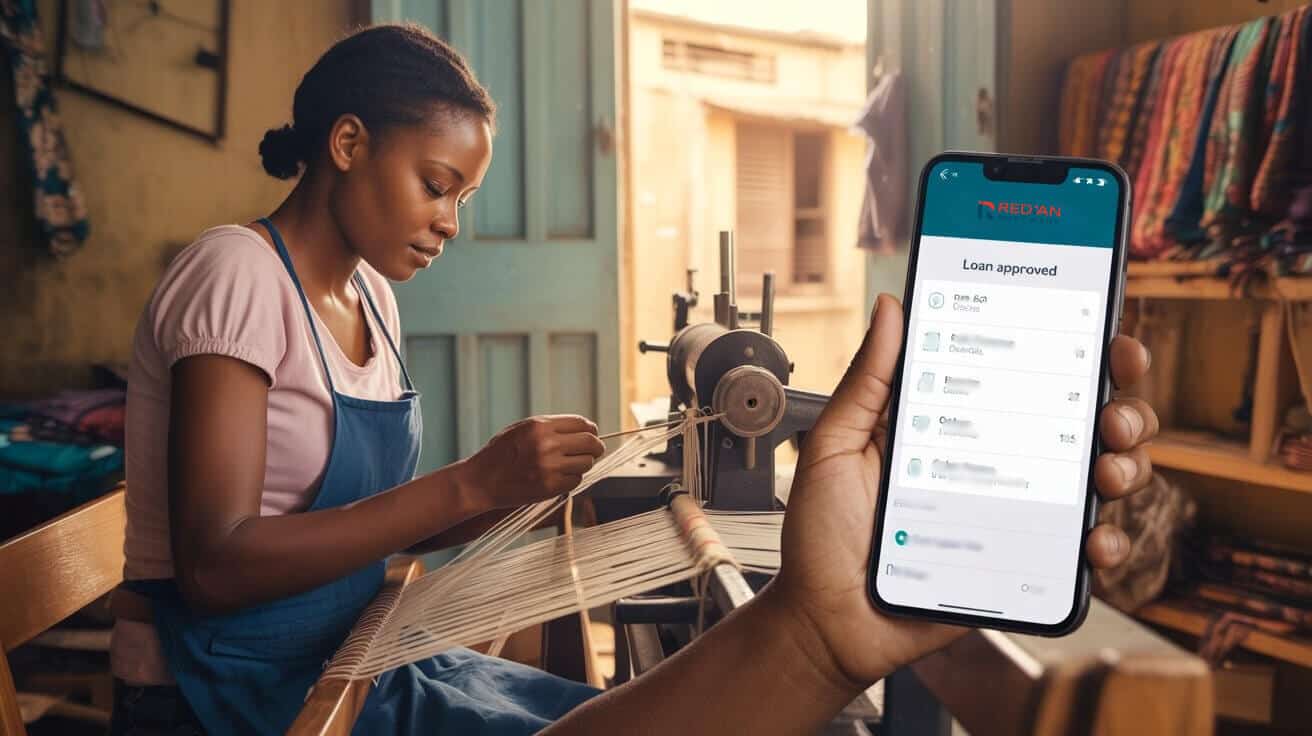

A digital lending platform is, at its core, a decisioning system wrapped around a distribution channel. The distribution channel is the phone — feature or smart, USSD or app — and the decisioning system replaces the loan officer with data: mobile money history, airtime top-up patterns, GPS, device metadata, social graph signals, utility payments, and increasingly, voluntary employer or payroll integrations.

This shift collapses the cost structure of lending in three ways. Origination moves from branch to handset. Underwriting moves from manual file review to automated scoring. Disbursement and repayment move from cash and cheque to instant wallet transfer. A loan that once took six weeks to approve and required a guarantor can now be priced, approved, and credited in under two minutes.

For the borrower, that means credit available at the moment of need — school fees, a stock-up for the kiosk, an emergency hospital bill. For the lender, it means a unit economics model that finally works at small ticket sizes. And for the technology partner, it means the underlying platform — the loan management system, the scoring engine, the integration fabric — becomes the single most important asset in the business.

Redian has been building exactly that fabric for African banks, microfinance institutions, and aggregators for nearly a decade. Our loan management system work and broader core banking practice sit at the centre of this transformation.

Mobile money: the rail that made lending possible

Digital lending in Africa does not exist without mobile money. M-Pesa serves over 51 million customers across seven African markets and remains the canonical example, but the pattern has been replicated across MTN MoMo, Airtel Money, Orange Money, and dozens of national wallets. In Sub-Saharan Africa, mobile money accounts now outnumber traditional bank accounts.

The continent holds nearly 70 percent of the world's roughly $1 trillion mobile money market. More importantly, mobile money is no longer just a payments rail. The share of mobile money services offering savings rose from 39 percent in 2022 to 44 percent in 2023, and microinsurance has surged alongside. For millions of women in Kenya, Uganda, and Zambia, a mobile money account is the first formal financial relationship of their lives — and the first usable credit record.

That credit record is what powers digital lending. A two-year history of regular wallet inflows, peer transfers, and bill payments tells an underwriter more about a market trader's ability to repay than any payslip ever could. Platforms that can ingest, normalise, and score that data — at speed and at the regulator's required audit standard — win the market.

The architecture that holds it together

Building a credible digital lending platform for the African market is not a single-product exercise. It is a stack. Done well, it includes:

- A loan origination layer with USSD, app, web, and agent channels — so the same customer can apply from a $30 feature phone or a flagship Android.

- A decisioning engine that combines rules, traditional credit bureau data where available, and alternative-data ML scoring for thin-file borrowers.

- A loan management core that handles disbursement, repayments, restructures, write-offs, and provisioning under the local regulator's classification rules.

- Deep integrations into mobile money operators, agency banking networks, payment switches, and where relevant, central bank reporting endpoints.

- A collections and recovery workflow that respects consumer protection rules and supports soft, digital-first follow-ups before escalation.

Pulling this together is where most in-house teams stall. The data plumbing alone — mobile money APIs, KYC providers, fraud screening, sanctions lists — can consume a year of engineering capacity. Our BFSI practice and custom software development teams have built these stacks for banks and aggregators across Kenya, Cameroon, Nigeria, and the wider region, and the reusable components shave months off go-to-market.

What the leading markets look like

Kenya remains the reference market — high mobile money penetration, mature regulator, deep ecosystem of digital lenders, and a credit bureau infrastructure that, while imperfect, is functional. Nigeria has scale: a population large enough that even modest penetration produces a business. Egypt is moving fast on regulatory clarity around digital banking and BNPL. South Africa has the most sophisticated credit infrastructure and the most demanding compliance bar.

Each market has its own quirks. Kenyan regulators have tightened rules on digital lender registration and pricing disclosure. Nigerian regulators have moved against unlicensed loan apps with aggressive collection practices. South African affordability rules under the National Credit Act require granular income and expenditure verification. A platform built once for one market will not survive the others without a configurable rules engine and a deliberate localisation strategy.

This is precisely why we approach every digital lending engagement as a platform conversation, not a product conversation. Configurable products, configurable workflows, configurable regulatory reporting — built on top of a stable core. Our core banking work in Cameroon and InsureMe aggregator build in Kenya reflect this discipline.

The role of AI and alternative data

The most interesting frontier in African digital lending is not the channel — that fight is largely won — but the underwriting. Thin-file and no-file borrowers dominate the addressable market, and traditional credit scoring simply cannot rate them. Machine learning models trained on mobile money behaviour, device data, behavioural biometrics, and repayment history from prior digital loans are now doing the work that bureau scores cannot.

Done responsibly, this approach extends credit to people who have never had it. Done carelessly, it produces opaque, hard-to-audit decisions that regulators will eventually push back on. The right architecture treats the model as one input into an explainable decision, keeps a human reviewer in the loop for edge cases, and maintains the audit trail that supervisors expect.

Redian's AI/ML consulting and AI/ML development teams work with BFSI clients on exactly this — building scoring engines, fraud models, and pricing systems that are accurate, explainable, and defensible in front of a regulator. For insurers entering the lending-adjacent space, our ML pricing and rating engine work follows the same principles.

The risks that come with the upside

Speed of disbursement is a feature for borrowers and a hazard for lenders. The same digital channel that approves a loan in 90 seconds can approve fraud in 90 seconds. Synthetic identities, SIM swap attacks, account takeovers, and coordinated default rings are real and growing. Any serious platform needs device fingerprinting, velocity rules, behavioural analytics, and cross-lender data sharing where regulators permit it.

Consumer protection is the other front. Predatory pricing, aggressive collections, and contact-list harvesting have drawn regulator action across multiple markets, and the long-term winners will be the providers who treat ethical lending as a competitive moat rather than a compliance tax. Transparent pricing, fair restructuring terms, and digital-first soft collections protect both the customer and the licence.

What the next five years look like

Three shifts are already visible. First, embedded lending: credit issued at the point of need inside a marketplace, ride-hailing app, or agri-input platform, with the lender invisible behind an API. Second, SME lending at scale: the merchant side of mobile money is now mature enough that working capital for kiosks, traders, and small manufacturers is a credible product, not a pilot. Third, cross-border: pan-African payment switches and harmonisation efforts will eventually make multi-market lending operationally viable for institutions ready for it.

For banks, microfinance institutions, and fintechs across the continent, the strategic question is no longer whether to build a digital lending capability. It is how to build one that scales, complies, and competes — and which parts to build in-house versus partner for.

Build with Redian

We have spent the better part of a decade building the digital lending and core banking stack for institutions across Africa, the Middle East, and beyond — from greenfield core banking deployments to ML-driven pricing engines and mobile-first origination journeys. If you are scoping a digital lending platform, modernising a legacy loan book, or extending an existing core into mobile money rails, our banking solutions team can help you move from blueprint to live deployment without losing time to the wrong architectural choices.

Stay current with our insights

One monthly email. Banking, insurance, AI/ML and CRM field notes. No spam.

We respect your privacy. Read our Privacy Policy.

Keep reading

More from Insights

Insights

How to organize your IT Department especially if you are starting out

The right tools make for successful IT staff augmentation. Benefit from increased agility, specialized skills, and cost-effectiveness with this strategy.

27 Nov 2023

Insights

Best practices for implementing Core Banking System for Banks & Micro-finance institutions

Discover key tips on how to upgrade your bank or micro-finance institution with a seamless core banking system.

20 Nov 2023

Insights

How an ROI-Focused Inventory System Transform Supply Chains

Whether on-premise or cloud-based, our cost-effective IMS system revolutionizes supply chains, boosting efficiency for a seamless experience.

11 Jul 2021

Build with Redian

Have a similar build in mind?

We've shipped insights systems for banks, insurers, brokers, MFIs, SACCOs and enterprises across the USA, UK, Africa, UAE and India. Book a 30-min call with a senior engineer — no pitch deck, just a sharp first read on your initiative.

- CMMI Level 3 Appraised · ISO Certified delivery

- 1 business day response · NDA on request

- Senior engineers, not sales — first call